We close the financial year 2025-26 as we began it, navigating uncertainty with a clear eye on what endures. The past quarter has been marked by one of the more challenging backdrop of events in recent memory: a major geopolitical conflict reshaping energy markets, persistent FII outflows, and a Nifty that has posted its third consecutive monthly decline. Investor anxiety is understandable.

However, anxiety and analysis are different things, and it is the latter that must guide decisions.

The Oil Shock: What It Means For India

The escalation involving the United States, Israel, and Iran has pushed crude oil front month contracts above $100 per barrel, the first sustained breach of that level in several years. Approximately 20% of global seaborne oil trade flows through the Strait of Hormuz, and markets have appropriately priced in a near term supply premium. The natural question for Indian investors is: what does this mean for us?

India imports nearly 85% of its crude requirements, making it one of the more exposed major economies to an energy price shock. The immediate effects are familiar upward pressure on inflation, potential compression of corporate margins in energy intensive sectors, and a slight widening of the current account deficit. These are real headwinds and we do not dismiss them.

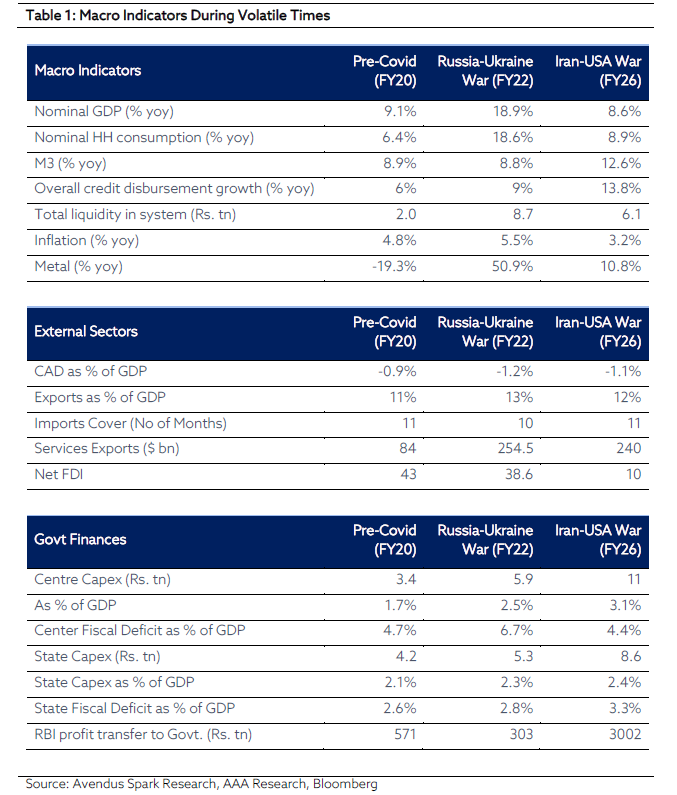

However, context matters enormously. Our base case, consistent with the assessment of most credible forecasters, is that this disruption is measured in weeks rather than quarters. A temporary oil shock is fundamentally different from a structural one. Unlike earlier stress episodes, India is entering this phase with significantly stronger macro shock absorbers (Refer to Table 1). Growth remains resilient, supported by healthy money supply expansion and robust credit growth. Inflation is materially lower, providing room for policy flexibility. External balances remain stable, with comfortable forex import cover, while services exports continue to provide a steady cushion.

Equally important, public capex has scaled up meaningfully at both the Centre and state levels, reinforcing domestic growth momentum. The Centre’s fiscal position is stronger compared to the Russia-Ukraine period, and the system benefits from improved liquidity conditions along with a higher RBI surplus transfer. Put simply, the foundation is stronger. This gives India a far greater ability to absorb short term commodity volatility without allowing it to evolve into a broader macro disruption something that differentiates the current phase from past crises.

What if the oil prices remains high for a longer period

Every USD10/bbl jump in oil prices widens India’s CAD 0.41% of GDP. In a stress scenario where oil sustains at USD 100/bbl through FY27, CAD could expand to ~2.3% of GDP which would still be within a manageable CAD range, especially when compared to past episodes where external imbalances triggered macro instability.

Will FII selling continue?

FIIs have been aggressive sellers in CY26, with net outflows of ~₹1.3 lakh crore, a headline that has understandably unsettled investors. However, in our view, the return of FII flows is a question of when, not if.

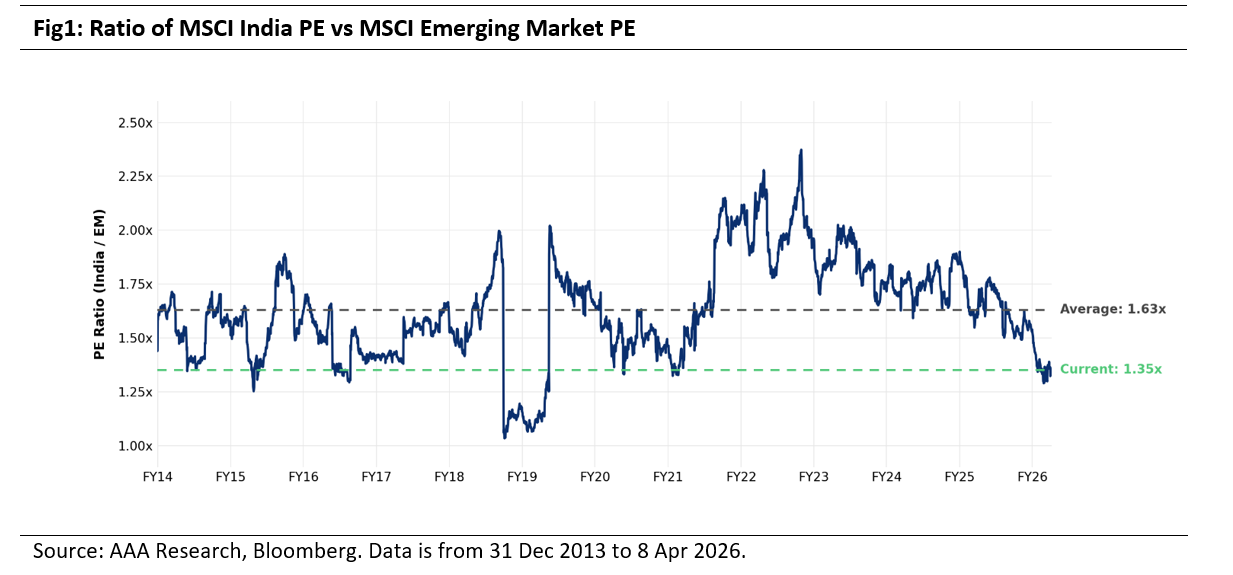

The valuation premium of MSCI India versus MSCI Emerging Markets has corrected meaningfully over the past year. P/E multiples is now approaching multi year support zones, levels that have historically marked important inflection points for India’s relative outperformance (Refer to Fig1).

As geopolitical uncertainty stabilises and India’s earnings growth advantage becomes more visible in a slowing global growth environment, the relative case for India strengthens further.

Valuation Linked Return Framework – What History Tells Us

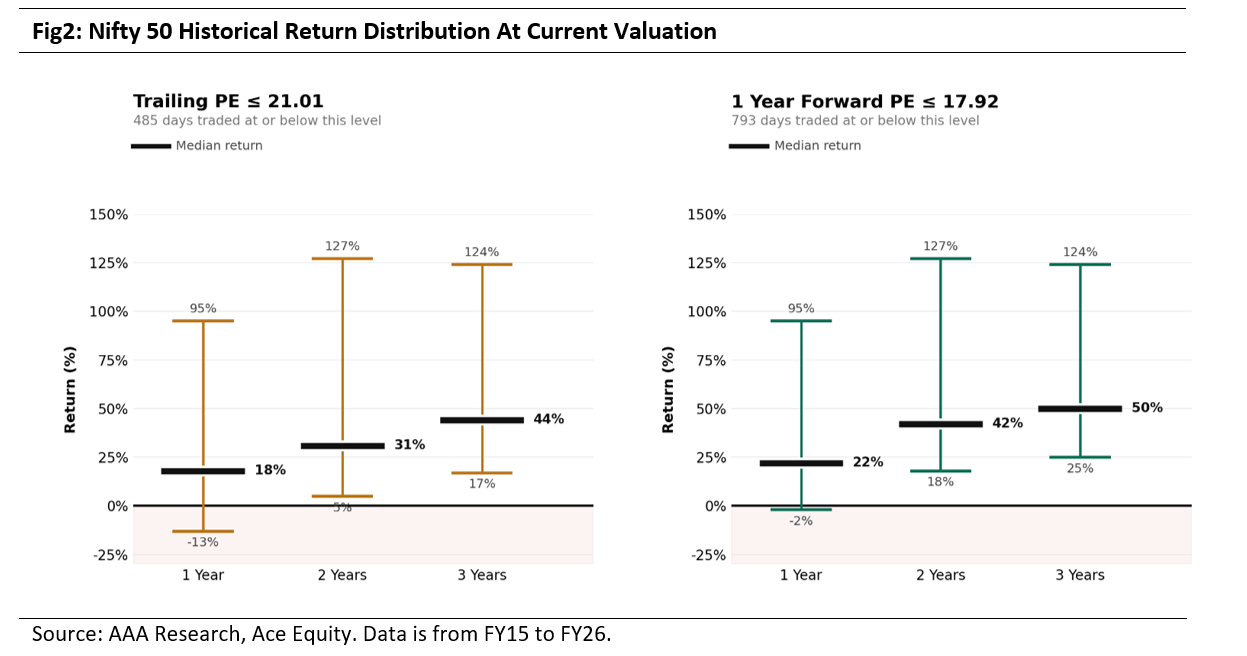

We examined historical return outcomes during periods when Nifty valuations were at or below current levels, both on trailing and forward P/E basis. The objective is to understand how markets have behaved from similar starting points.

The message from history is clear: current valuations offer a favourable entry point.

While short term volatility may persist, the probability of positive outcomes rises sharply with time horizon, with forward valuations indicating near zero downside risk.

Over the last 11 years, the NIFTY 50 traded at or below 21x trailing P/E on 485 trading days. Historically, investing at these valuation levels has resulted in positive returns 90% of the time over the subsequent 1 year, and 100% of the time over 2 to 3 year holding periods. Even in less favorable outcomes, downside has been relatively contained, with the worst 1 year return at -13%, while median returns were 18% for 1 year, 31% for 2 years, and 44% for 3 years, indicating an attractive risk reward profile from comparable valuation entry points (Refer to Fig 2).

Over the last 11 years, the NIFTY 50 traded at or below 18x forward P/E on 793 trading days. Historical outcomes from these valuation levels have been even more compelling, with a 99% probability of positive returns over the subsequent 1 year and no instances of negative returns across 2 to 3 year holding periods. Downside risk has been minimal, with the worst observed 1 year return at approximately -2%, while median returns were 22% for 1 year, 40% for 2 years, and 50% for 3 years, reinforcing this valuation band as a high conviction accumulation zone (Refer to Fig 2).

How We Are Navigating This Phase

At AlfAccurate Advisors, our portfolios are constructed with a clear emphasis on resilience based on our 3M (Market Size, Market Share, Margin of Safety) approach. We continue to focus on businesses which enjoys market leadership, strong balance sheet and robust cash flows which are better positioned to navigate external shocks.

Our approach remains anchored in what we describe as QuAgile investing: combining quality with agility. This allows us to be disciplined in stock selection while remaining responsive to changing market conditions, particularly in managing valuations and portfolio positioning.

Sectoral Preferences

In the current environment, sector selection becomes critical, not just in identifying opportunities, but in consciously avoiding areas of structural risk. Oil marketing companies (OMCs) and aviation are among the most impacted sectors in a rising crude price scenario. Both face direct margin pressures, limited pricing flexibility (particularly for OMCs), and elevated earnings volatility. Our portfolios have zero exposure to these sectors, reflecting our disciplined approach to risk management.

On the other hand, we continue to see favourable opportunities in sectors with strong earnings visibility and structural tailwinds. Automobiles and auto ancillaries remain well positioned, supported by demand recovery, premiumisation, and operating leverage benefits. Consumption oriented businesses, particularly discretionary, are likely to benefit from improving income dynamics and policy support, with potential for a sharper rebound as sentiment normalises. We remain constructive on banking and financials, where healthy credit growth, stable asset quality, and strong capital positions underpin sustained earnings delivery. Capital goods continue to stand out as a key structural theme, driven by the ongoing capex cycle across both public and private sectors.

The Investor Dilemma

A common question we are encountering from investors is whether this is the right time to invest or whether one should wait for greater clarity.

Our answer remains consistent: Good Price & Good News Never Come Together.

By the time uncertainties recede and the outlook appears clearer, markets tend to have already adjusted, often at higher valuations. The challenge for investors, therefore, is not timing the market perfectly, but maintaining discipline during periods of discomfort.

Our Advice to Investors

In such environments, we believe investors should avoid binary decisions and instead adopt a measured approach. Staggered deployment of capital, alignment with long term investment horizons, and a continued focus on business quality remain critical. Volatility should be viewed as part of the investment journey rather than a signal to deviate from a well defined strategy.

DISCLAIMER: This document is not for public distribution and has been furnished to you solely for your information and may not be reproduced or redistributed to any other person. The manner of circulation and distribution of this document may be restricted by law or regulation in certain countries, including the United States. Persons into whose possession this document may come are required to inform themselves of, and to observe, such restrictions. This material is for the personal information of the authorized recipient, and we are not soliciting any action based upon it. This report is not to be construed as an offer to sell or the solicitation of an offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. No person associated with AlfAccurate Advisors Pvt Ltd is obligated to call or initiate contact with you for the purposes of elaborating or following up on the information contained in this document. The material is based upon information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon. Neither AlfAccurate Advisors Pvt Ltd., nor any person connected with it, accepts any liability arising from the use of this document. The recipient of this material should rely on their own investigations and take their own professional advice. Opinions expressed are our current opinions as of the date appearing on this material only. While we endeavour to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so. Prospective investors and others are cautioned that any forward-looking statements are not predictions and may be subject to change without notice. We and our affiliates, officers, directors, and employees worldwide, including persons involved in the preparation or issuance of this material may; (a) from time to time, have long or short positions in, and buy or sell the securities thereof, of company (is) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company (is) discussed herein or may perform or seek to perform investment banking services for such company(is)or act as advisor or lender / borrower to such company(is) or have other potential conflict of interest with respect to any recommendation and related information and opinions. The same persons may have acted upon the information contained here. No part of this material may be duplicated in any form and/or redistributed without AlfAccurate Advisors Pvt Ltd.’s prior written consent. No part of this document may be distributed in Canada or used by private customers in the United Kingdom. In so far as this report includes current or historical information, it is believed to be reliable, although its accuracy and completeness cannot be guaranteed.